The financial markets have changed: successful companies can now stay private forever.

Stripe is the canonical example. It was founded in 2010, and fifteen years later it is still privately held and worth around $91bn dollars. By contrast, Apple was founded in 1976 and went public in 1980; after a day of trading the company was worth around $1.2bn (or about $3bn adjusted for inflation). Amazon was founded in 1994 and went public in 1997 with a market cap of around $440m (about $1bn adjusted for inflation).

In 1980 there were far fewer options for private companies that wanted to raise $1bn in capital. Now it’s almost prosaic; in April SoftBank announced a $40bn cash infusion into OpenAI.

The availability of private capital, the 2012 JOBS act*, and the accepted startup wisdom that post Sarbanes-Oxley you don’t want to be a public company CEO, means that more companies will stay private.

So what are the implications of this new universe for startup employees, VC investors, and public market investors?

It’s a bad time to create a mediocre company. The excellent companies that remain private (OpenAI, SpaceX, Anduril, and so forth) have enough liquidity and demand in secondary markets so that founders, early employees, and early investors can sell their shares when they want.

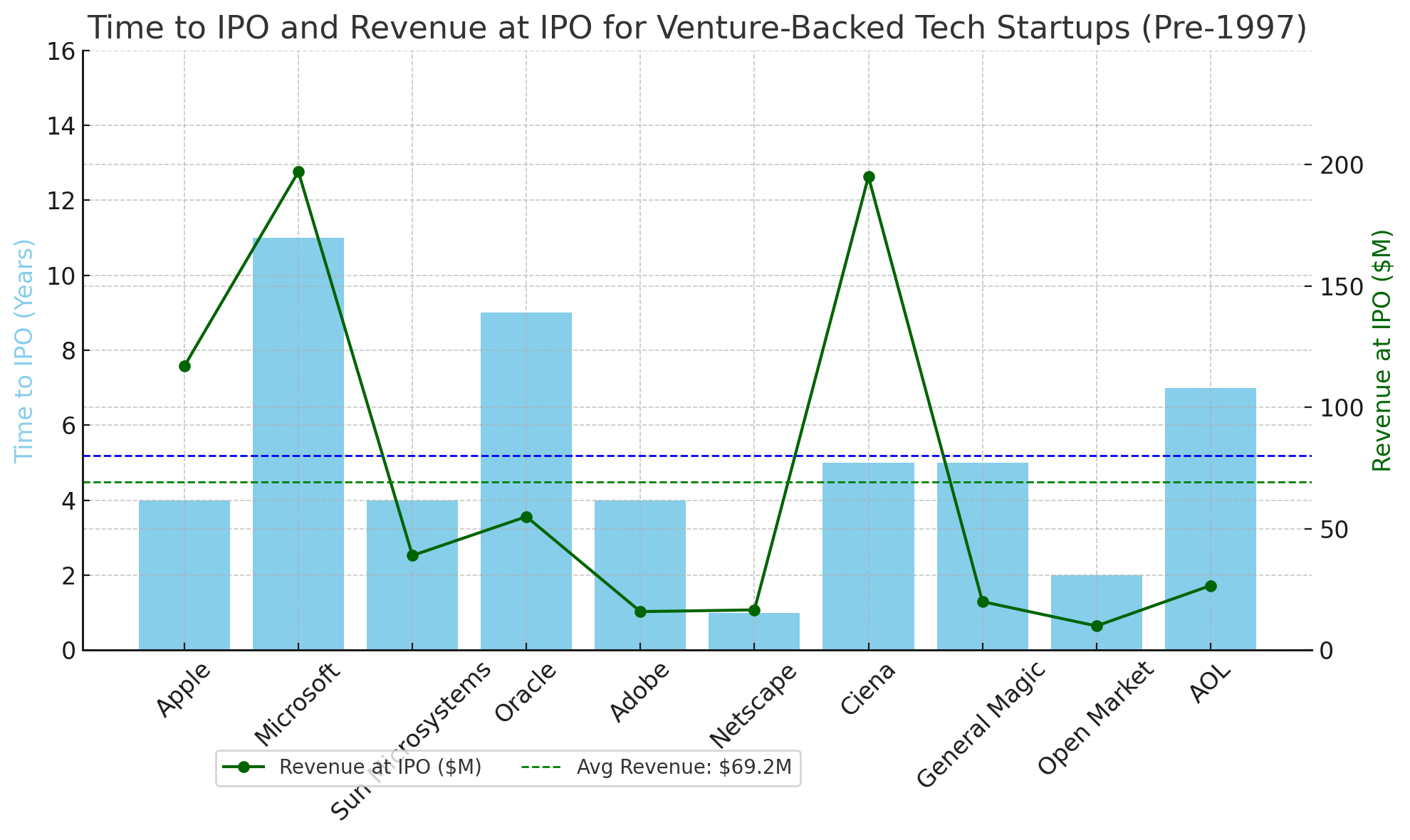

As an early stage investor, I wish it were easier and more palatable for companies to go public. I had ChatGPT produce a chart of notable pre-1997 IPOs — it’s a small sample, but it suggests that before 1997 the breakout companies would go public after about six years and with an average of about $60m in revenue!

But the banking system was different then and it’s not actually clear that allowing companies to go public earlier and with less scrutiny was for the best. We haven’t had another public dot-com bubble since 1999, unless you count whatever happened with crypto ICOs in 2020 and 2021.

Not many companies have gone public over the last several years, and VCs have been quick to point out that this makes it hard to return cash to their investors! Of course historically, around three-quarters of venture outcomes have come from M&A, and the recent US administration’s hard line against M&A is probably more to blame for the VC liquidity problems than the lack of IPOs.

Tom Tunguz posted a chart of M&A activity that really puts a spotlight on it (I quipped: Silicon Valley’s political change of heart in one chart).

I started working on this post about two months ago, and I thought I was going to propose a serious problem for early stage VC (that companies stay private too long) and a radical solution (to use the private markets like public markets), but after talking with a number of veterans and chewing on all of these ideas, I think the real problem is that creating VC returns is really hard and there are a lot of people trying to do it.

I just watched Eric Newcomer’s interview with Bloomberg Capital’s Roy Bahat, in which Roy says:

“I think [VC] is more the same than different. It's all about finding the outliers, and the outliers are very hard to find.”

Well said, Roy.

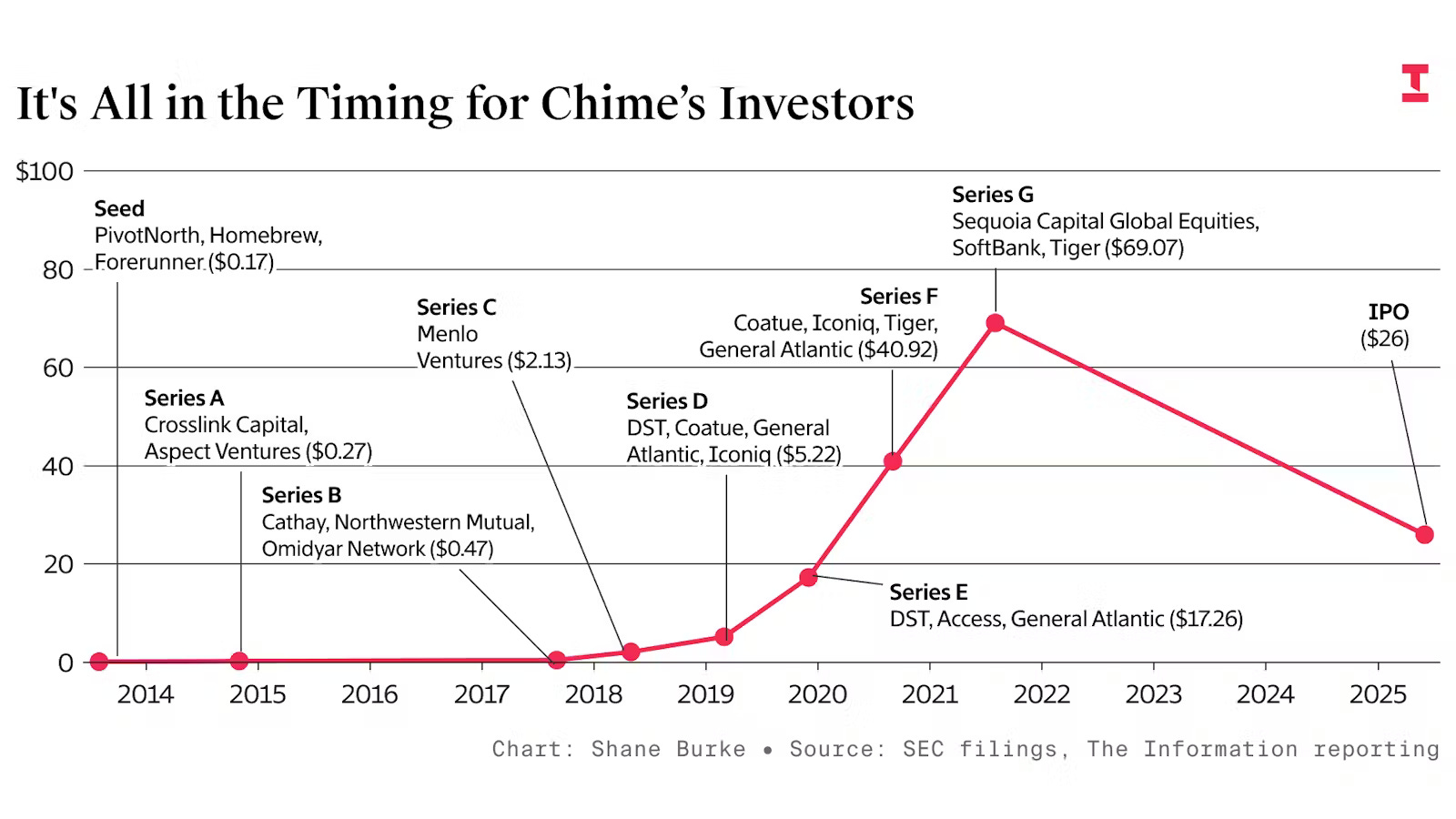

If you have shares in a great company, there will be opportunities to sell those shares and as a VC you’ll have to figure out when to sell those shares to create the best outcome for your LPs. It might be well before the company goes public. The Information published a chart about the recent Chime IPO that illustrates this idea perfectly:

If you have shares in a company that is valued incorrectly, you need to figure out how to value those shares correctly or risk losing the entire investment (because other investors are smarter than you think and they won’t bail you out). If you have shares in a company that is never going to be big enough to go public, you have to be adept at getting the entrepreneur to understand that and at finding a larger company that can and will acquire it.

Many of today’s VCs are very good at helping build products and companies because they have excellent experience doing it. But good fund management is different than building a company, and knowing how to create liquidity is a key part of that skill set.

* The 2012 JOBS act changed the limit on the number of shareholders allowed in a private company from 500 to 2,000. Microsoft was forced to go public because they ran into the 500 shareholder cap, but today’s lawyers are more clever, and the 2,000 shareholder limit is high enough, that this is no longer a forcing function.